How Could Blockchain Transform Your Business?

Blockchain has innovative implications for business operations. From accounting to operation management, industry leaders have a growing consensus that this will likely impact all significant work areas – and change has already begun. Blockchain can potentially add $1.76 trillion to the global economy by 2030.

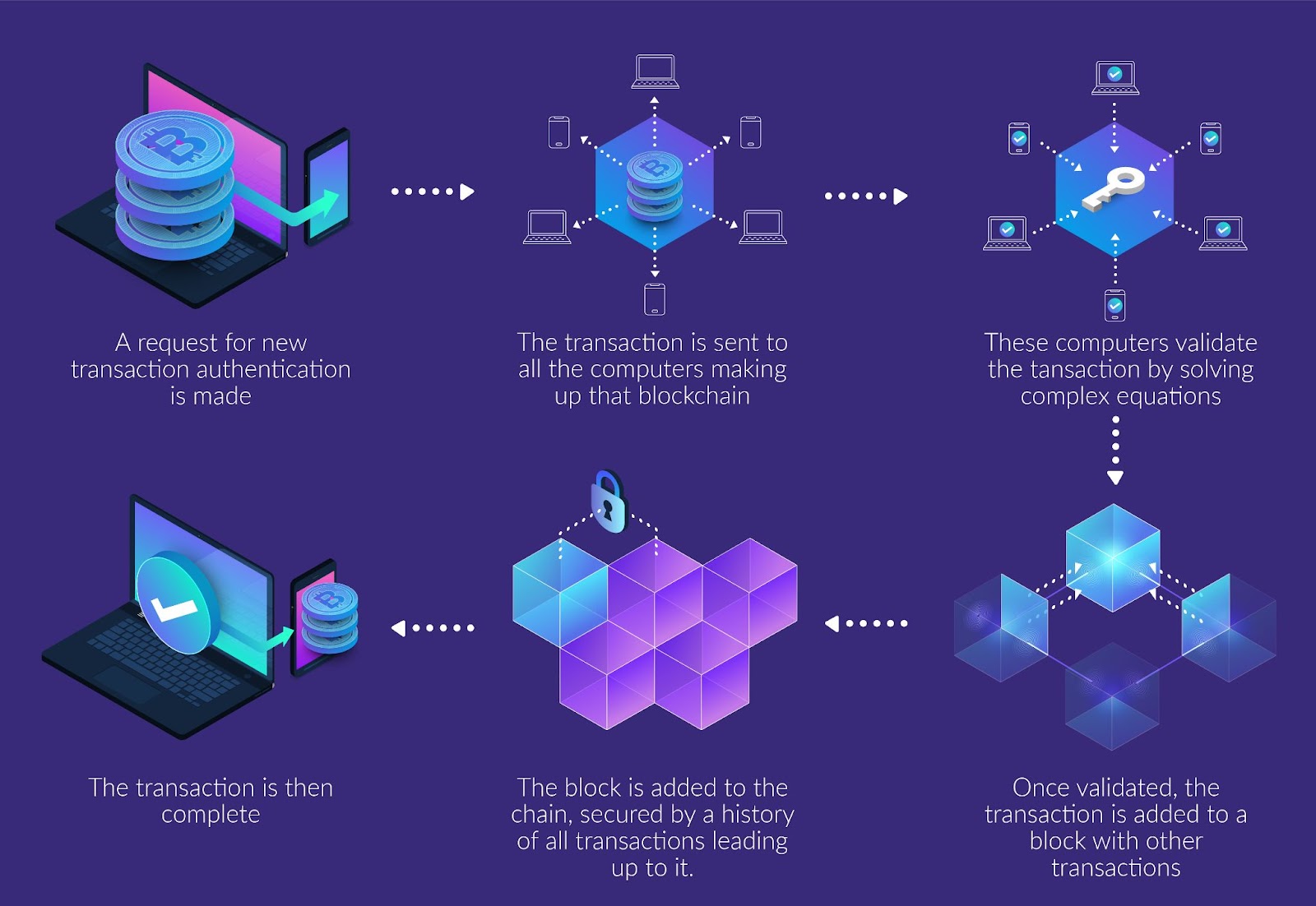

The technology systematically tracks transactions from beginning to end without consulting a central authority to store the transactions or encrypt the data without human intervention. Instead, the blockchain provides transparency into what happened in transaction history through classification. In addition, the blockchain being immutable, this information is secure.

This "digital ledger" empower creators and advocates to turn the script on typical organizational processes in various exciting ways.

Find out some of the business applications:

Asset protection

Cybercrime is estimated to cost US$6 trillion in global damages in 2021, which is expected to rise to US$10.5 trillion annually by 2025. Cybercrime is a serious problem, but blockchain could bring you some relief.

Inherently transparent, immutable, and decentralized, the technology offers greater transaction security. Blockchains store data using sophisticated mathematical and software rules that are nearly impossible for attackers to manipulate. Each block added to the chain carries a hardware cryptographic reference to the previous block. This reference is part of a complicated math problem that needs to be solved to fit the next block into the chain. The process creates a unique encrypted digital fingerprint called a "hash" that is secure and highly tamper-proof.

However, despite its many advantages, blockchain is not a magic bullet to prevent cybercrime. Unfortunately, blockchains still work on operating systems that have exploitable vulnerabilities. Therefore, to mitigate end-user vulnerabilities, organizations must ensure that their external data sources are secure as they are not on the blockchain.

Eliminating the middle-man

Professionals involved in banking, contracts, invoicing, or any other business process that consists in being a third party in a transaction may be affected by the growing adoption of blockchain.

Blockchain cryptology replaces third-party intermediaries as trustees. And by using math instead of intermediaries, blockchain can help reduce overhead and hassle for businesses or individuals when trading assets.

If you work in this field, it might be thoughtful to arm yourself with a thorough understanding of the cryptocurrency assets that are created, stored, transmitted, and verified on the blockchain to realize their potential.

Reducing operating costs

Blockchain facilitates businesses to circulate payments through systematic sets of rules labeled "smart contracts". These contracts are programmed into a blockchain, and the smart contract will automatically trigger the following appropriate action when a pre-determined condition is met. This process eliminates the need for brokers, trustees, and other financial intermediaries. Moreover, the blockchain is updated during the execution of the contract, and the transaction cannot be modified.

Since all actions related to a given smart contract are transparent and recorded, the technology generally reduces tracking and reconciliation costs. This is very promising for global companies, as essential administrative functions such as payroll can be performed seamlessly in different countries. It only becomes more relevant in the context of an increasingly decentralized global workforce.

By establishing irreversible and enforceable rights and obligations for all parties involved, smart contracts can also help facilitate the employment of the estimated 1.7 billion people worldwide who do not have a bank account with a recognized financial institution. Additionally, employers and employees would benefit from making payments in a widely accepted cryptocurrency, which is transferred directly to the individual and not through a third-party intermediary.

Supply chain tracking

Business owners often don't see all the players in the supply chain, but blockchain technology creates transparency. In the food industry, for example, it is imperative to have solid records tracing each product back to its source in case of a problem. For example, Walmart has partnered with IBM Food Trust in a blockchain project to track fresh produce and other groceries. Walmart Canada used a blockchain supply chain and invoicing platform to manage half a million shipments annually and reduced shipping discrepancies by 97%.

Supply chain transparency also helps verify things like part authenticity and ethical sourcing. By leveraging blockchain technology, a business can digitally create durable and verifiable records for stakeholders and investors. Transparent and effective audits are one of the most common ways to improve supply chain execution.

New opportunities for blockchain in business

Blockchain is the backbone that enables cryptocurrency transactions, and the technology finds its way into countless facets of our professional and personal lives. Other applications include insurance claims processing, virtual litigation, environmental, social, and corporate governance monitoring, drone air traffic control, and increasing currency flow efficiency. It's a brave new world with endless opportunities for companies willing to embrace technology.